We are team of experienced professionals who add value to their business. Our clients can expect:

A fresh and proactive approach to their accounts and tax planning

A friendly and personal service

Innovative solutions to requirements

About US

Get link

Facebook

X

Pinterest

Email

Other Apps

We are team of experienced professionals who add value to their business. Our clients can expect: A fresh and proactive approach to their accounts and tax planning A friendly and personal service Innovative solutions to requirements

IF INCOME OF RS 50,000 PER MONTH THEN NO TDS A)STANDARD DEDUCTION FROM GROSS SALARY UNDER SECTION 16 (ia) of (“The Act”) As per the provision prior to amendment A deduction of Rs 40,000 or Amount of salary (whichever is less). i.e. Rs 40,000 As per amendment made in this provision w.e.t. A .Y. 2020-21 The deduction has been raised from Rs 40,000 to Rs 50,000 . i.e. Rs 50,000 B)REBATE FROM INCOME TAX TO A RESIDENT INDIVIDUAL UNDER SECTION 87A of (“the Act”) As per provision prior to amendment Rebate u/s 87 A is available if – i) His total taxable income upto Rs 3,50,000 Quantum of rebate is – Amount of income -tax payable or Rs 2500 (whichever is less) i.e Rs 2500 As per amendment made in...

Commissioner Has Power To Cancel Registration of Trust Amendment of Section 12AA of income tax act with effect from 1 st November 2019, provides that cancellation of registration can be on two grounds i. The Principal Commissioner or the commissioner is satisfied that activities of trust or institution are not genuine or are not being carried out in accordance with its objects AND & ii. Where a trust or an institution has been granted registration under section 12A and subsequently ,it is noticed that the trust or institution has violated requirements of any other law which was material for the purpose of achieving its objects , the principal commissioner or commissioner may, by...

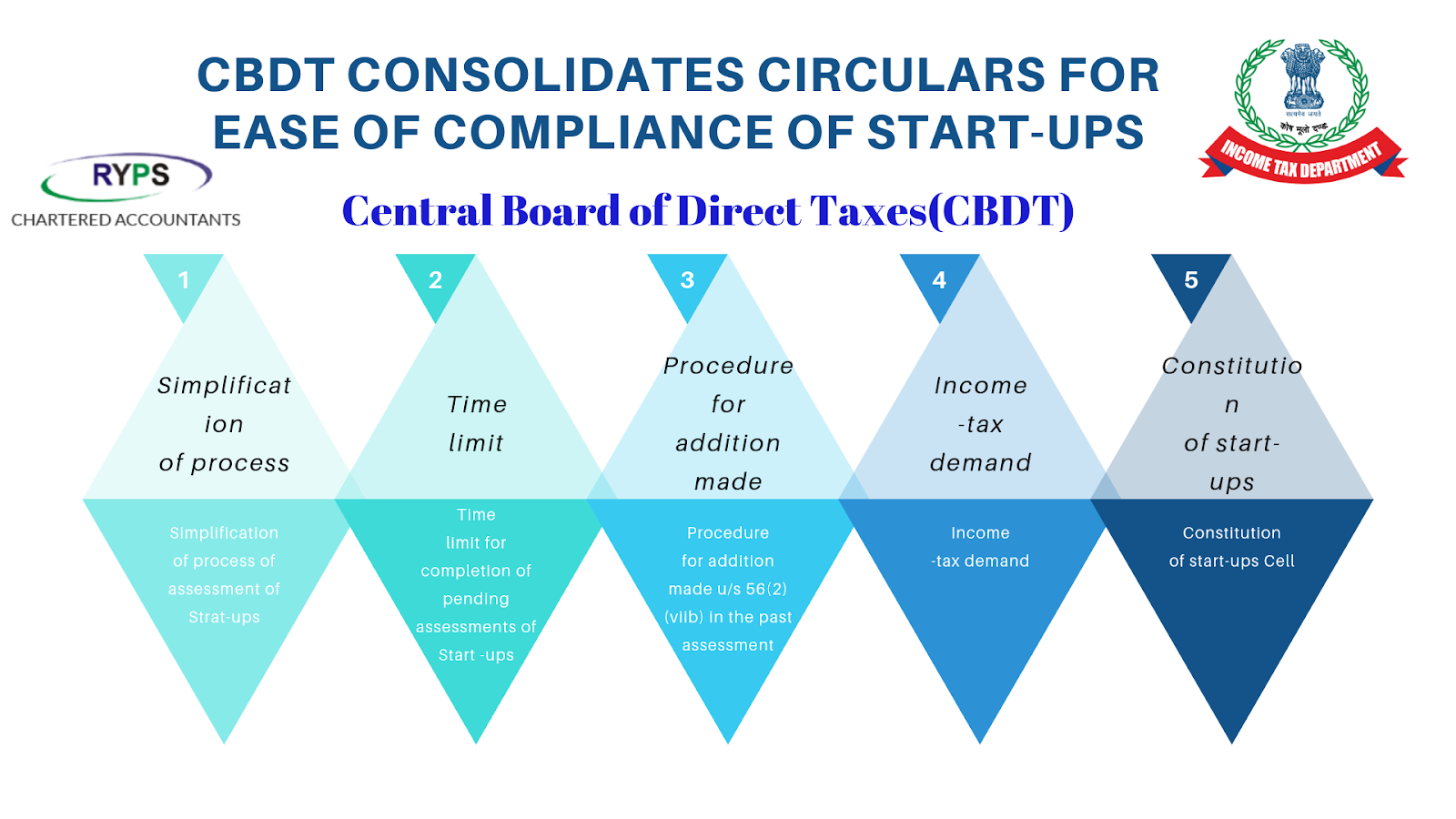

In order to provide hassle -free tax environment to the Start-ups. CBDT issued various circulars / clarifications on a series of announcement have been made by Finance Minister Smt. Nirmala Sitharaman in her General Budget 2019 and also on 23rd August 2019. The present circular inter alia highlights the following: - i) Simplification of process of assessment of Strat-ups – Circular No 16/2019 dated 7th of August 2019 provide for the simplified procedure of assessment of Start-ups recognized by DPIIT . the circular covered cases under “limited scrutiny “, cases where multiple issues including issue of section 56(2)(viib) were involved or cases where Form No 2was not filed by the start-ups entities. ii) Time limit for completion of pending assessments of Start -ups: All cases involving “ limited scrutiny “ were to be completed preferably by 30th September 2019 and the other cases of start-ups were to be disposed off on priority preferably by 31st October 2019. iii) Proc...

Comments

Post a Comment